Welcome to the fourth Weekly Market Dossier of 2025!

This week…

Trump was sworn in

Tariffs were pushed further down the docket

Trump’s pen was busy

EU and UK data was uplifting

Central bankers said some stuff

Crypto regulators formed groups

Japan raised rates

Stocks made a new ATH

Let’s dig into these and more!

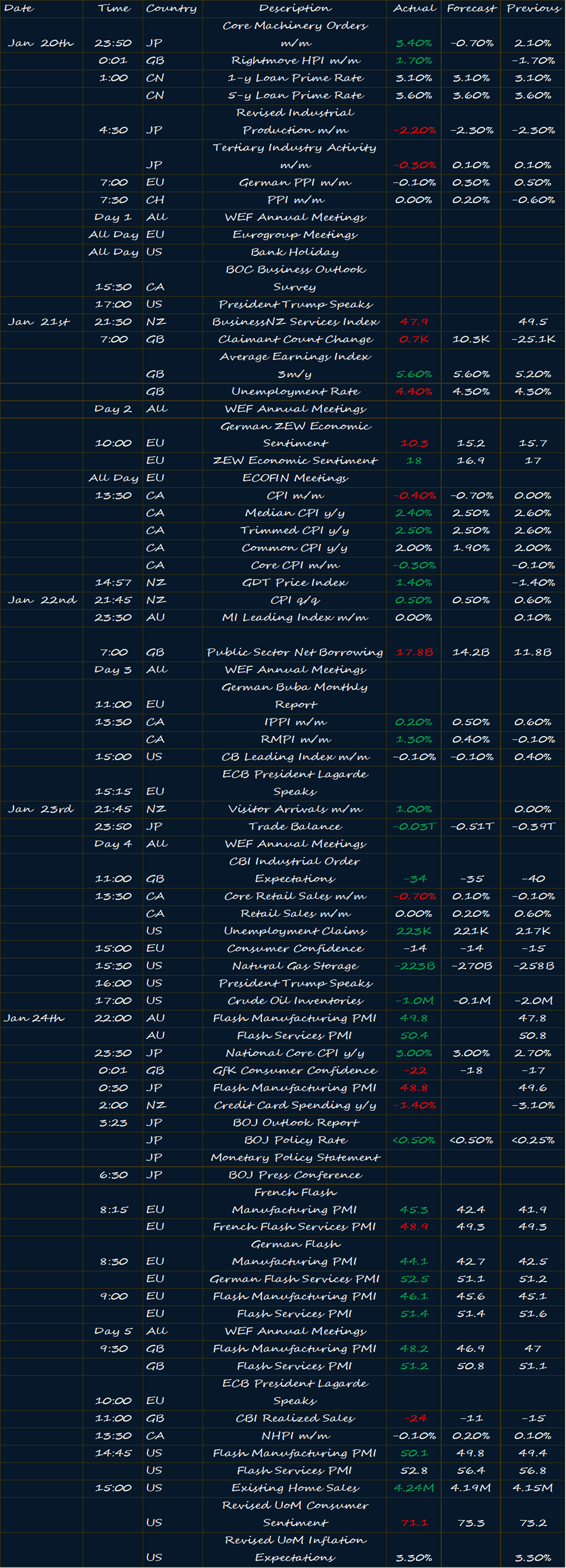

🌐 Economic Releases

In Japan, Core Machinery Orders saw a significant increase of 3.40%. However, Revised Industrial Production and Tertiary Industry Activity both decreased, with Revised Industrial Production falling by 2.20% and Tertiary Industry Activity declining by 0.30%. The Trade Balance also shows a deficit at -0.03T. Towards the end of the week, Japan’s National Core CPI increased to 3.00%, and the BOJ raised the policy rate to 0.50%—the highest level since 2008.

The United Kingdom’s Rightmove HPI increased by 1.70%. However, there are several concerning indicators such as an increase in the Claimant Count by 0.7K, an increase in the Unemployment Rate to 4.40%, and an increase in the Public Sector Net Borrowing to 17.8B. Average Earnings also increased to 5.60% which was welcome news. There was a decrease in the CBI Industrial Order Expectations to -34. The GfK Consumer Confidence decreased to -22. The CBI Realized Sales also decreased to -24. Despite these negative results, both the Flash Manufacturing and Services PMIs showed increases with the Flash Manufacturing PMI at 48.2 and the Flash Services PMI at 51.2.

In China, the 1-year and 5-year Loan Prime Rates remained stable at 3.10% and 3.60%, respectively.

In the Eurozone, the German PPI decreased by 0.10%. The German ZEW Economic Sentiment decreased to 10.3, and the Eurozone’s ZEW Economic Sentiment also decreased to 18. The Flash Manufacturing PMI for the Eurozone showed an increase to 46.1, and the Flash Services PMI also rose to 51.4.

Switzerland’s PPI also showed a decrease, moving to 0.00%.

In Canada, CPI data showed decreases across the board with the CPI m/m decreasing to -0.40%, Median CPI y/y to 2.40%, Trimmed CPI y/y to 2.50%, and Common CPI y/y to 2.00%. Additionally, the Core CPI m/m decreased to -0.30%. There was also a decrease in the Core Retail Sales m/m to -0.70%. The IPPI m/m decreased to 0.20% while the RMPI m/m increased to 1.30%. The NHPI m/m showed a decrease to -0.10%.

New Zealand's BusinessNZ Services Index is at 47.9. The GDT Price Index increased by 1.40%. There was also a decrease in the Credit Card Spending y/y to -1.40%. The CPI q/q decreased to 0.50%. The Visitor Arrivals m/m increased to 1.00%.

Australia’s MI Leading Index remained unchanged at 0.00%. The Flash Manufacturing PMI decreased to 49.8, while the Flash Services PMI increased to 50.4.

In the United States, the CB Leading Index decreased to -0.10%. There was a decrease in the Unemployment Claims to 223K, and Existing Home Sales increased to 4.24M. Additionally, the Flash Manufacturing PMI increased to 50.1 while the Flash Services PMI decreased to 52.86. The UoM Consumer Sentiment was revised down to 71.1. The Natural Gas Storage decreased to -223B and Crude Oil Inventories decreased to -1.0M.

💵 Central Banks

ECB's Holzmann expresses a cautious stance, emphasizing the risk of cutting rates too early while inflation remains high. His comments suggest a concern that premature easing could force the ECB to reverse course and hike rates again. He would rather wait longer before cutting rates until he is persuaded by solid arguments. This reveals a hawkish position, prioritizing the fight against inflation over stimulating growth.

BOE's Woods is focused on potential regulatory changes to boost UK growth, suggesting the BOE is looking beyond monetary policy. This indicates that the central bank is open to collaborating with the government to explore other avenues to achieve economic improvement, and is recognizing the limitations of monetary tools alone.

ECB's Vujcic’s comments reveal a lack of major concern about FX movements, and that he anticipates an increase in household consumption. This suggests that he believes the current policy stance is appropriate and that he is optimistic about consumer spending. He also notes that the central bank engineered a soft landing, but that the "takeoff" will be hard, and he sees a clear risk of stagflation. This reveals a complex view, that, while confident in the current policy, recognizes the significant risks that remain.

ECB's Nagel presents a generally positive outlook, expressing confidence in the ECB's path to reach its 2% inflation target, while also indicating that policy decisions are not predetermined and that the ECB will act based on data. He views Germany as economically strong, and sees a need for stability in consumption and investment. This implies a belief that current monetary policy is working but that the ECB remains flexible and responsive to incoming data.

ECB's Villeroy conveys a sense of optimism about the progress against inflation while advocating for a steady pace of rate cuts, suggesting that aggressive cuts are not necessary at this time, but also doesn't exclude the possibility in the future. He also emphasizes the need for structural reform and sees the new US administration under Trump as a "wakeup call" for Europe. This implies a view that the fight against inflation is on track, but also sees the necessity of economic reform and that potential protectionist policies in the US should be a concern for Europe. Villeroy also comments on the financial situation in France, stating that the country is not at risk of being unable to finance itself, but there is the question of at what cost. He implies that markets will assess France's credibility. He believes that French growth will improve in 2026 and 2027.

ECB's President Lagarde’s remarks indicate that the ECB is not behind the curve on rate cuts. She emphasizes that gradual steps are appropriate and that the disinflationary process in Europe is continuing. She will also be attentive to energy prices. She notes that she expects no US tariffs and that this is a smart approach. She mentions that she will be attentive to the price of energy but hasn't anticipated decline in energy prices. She suggests that there are risks to downside on euro-area growth this year, but is confident that Eurozone inflation will be at the target by 2025. She highlights the consensus in Europe regarding capital markets and is not overly concerned by the export of inflation to Europe.

SNB's Chairman Schlegel states that he sees no need for a retail digital central bank currency, that monetary conditions in Switzerland are currently appropriate, and that the Swiss franc is a safe haven. He also said that he cannot exclude negative interest rates. He also states that while the current policy mix was very effective, they don't claim victory. He states that tariffs would not be good for Switzerland. These statements indicate a cautious approach, acknowledging ongoing risks even while monetary conditions are working as intended.

ECB's Escriva suggests a preference for waiting for hard data to confirm forecasts, while seeing a 25 bps rate cut next week as a likely scenario. This reveals a data-dependent approach but also indicates a leaning toward easing monetary policy.

ECB's Stourmaras states that possible US tariffs would speed up interest rate cuts in the Eurozone. He believes that rate cuts should be at the order of 25 bps each time to get close to 2% by the end of 2025. This indicates that US policy could significantly influence the ECB's decisions and that they would be responsive to a new trade environment.

ECB's Knot10... Knot's remarks suggest that if the recovery continues, there may not be a need for a stimulative mode, indicating that he does not think the economy needs further stimulus if the economy performs as expected. He believes that there are new downside risks from trade policy, and that data is encouraging, confirming the picture of a 2% return. He states that he sees little obstacle to another rate cut next week. This suggests a positive outlook for the near future, and that the ECB is likely to take further action to loosen monetary policy.

BOJ's Gov. Ueda’s comments provide an in-depth look at the BOJ's perspective. He believes that the BOJ has come closer to a neutral rate compared to when the policy rate was 0.25%. He views the economy and prices as being on track with their forecasts and that he sees inflation settling at 2% around FY2026. He also notes that there has been no shock in the market after the new US administration. He notes that uncertainties remain high over Trump tariff details. He states that he will be closely watching the impact of their recent rate hike. He emphasizes that there must be price stability while securing the value of the currency. Ueda's comments reveal a nuanced approach, cautiously optimistic about inflation trends but also mindful of risks and external shocks. He is focused on wage growth and is seeing a positive trend. He states that he will provide a view once details become clear regarding Trump's tariff policy. He does not believe that the BOJ is behind the curve.

You can read all the central bank speaker’s comments in the PDF below.

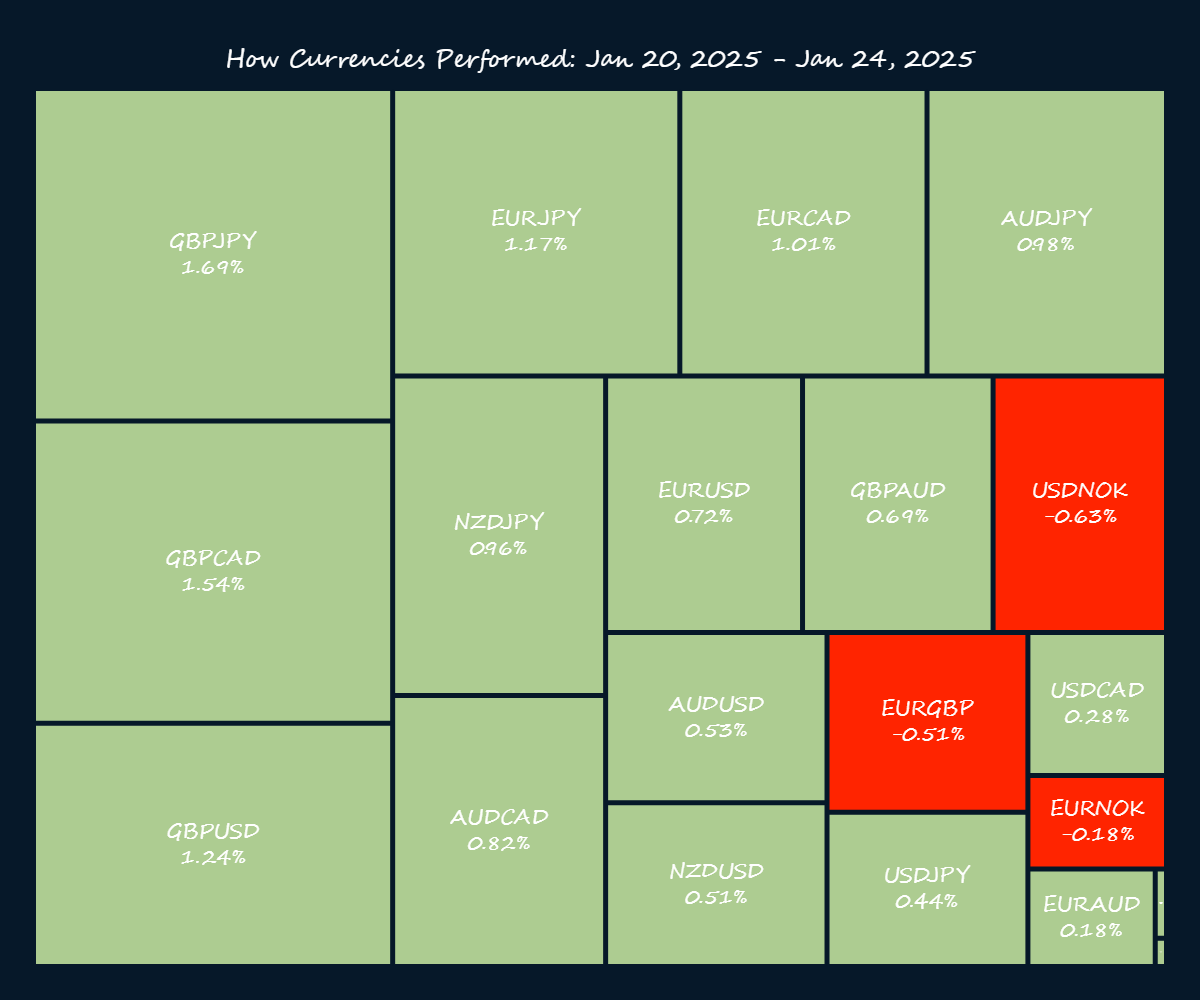

💱 Currencies

The broad theme in currencies this week was a dollar sell-off with the major beneficiaries being a dollar sell-off after a WSJ article, which was later backed by a Trump official, claimed that there would be no day-one Tariffs. Trump failed to mention tariffs in his inaugural speech, but later in his victory rally, he mentioned potential tariffs against Canada, Mexico and China. USDCAD whipsawed to end the week weaker against the dollar. Upbeat PMIs from the EU and UK also helped the dollar correction but the UK had better manufacturing PMIs which helped the EURGBP break below a range-bound top.

The main beneficiary of these developments was Cable which seems to have finally brushed past the fiscal worries from a fortnight ago. Reeves was on the tapes saying UK’s public finances were now in order and that she expects growth in future. On Thursday, 10-year gilts were back below US 10-year yields but Friday’s PMI put them back at a premium.

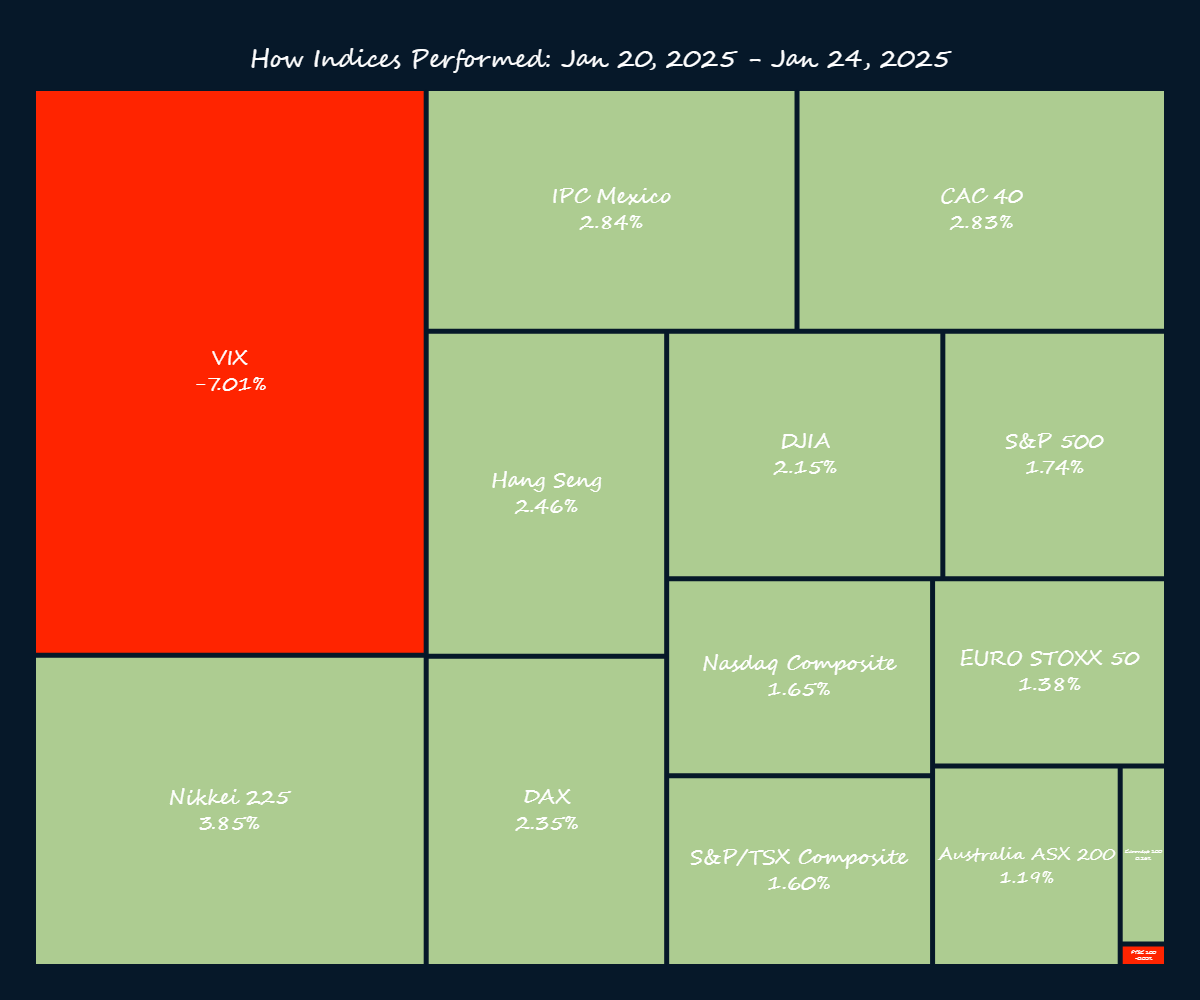

📉 Stocks

Stocks had a stellar week in what is touted to be the best inaugural response ever. VIX was down and all indices gained more than 1% apart from the Shanghai Composite and the FTSE 100. FTSE’s rise was driven by cheap pounds so the rise in Cable is partly to blame for its forestalled rally. However, stocks ended the week with some declines. The S&P 500 recorded its first record high of 1025 on Wednesday but ended the week with a 0.3% decline. Russell 2000 and Nasdaq shed 0.6% on Friday.

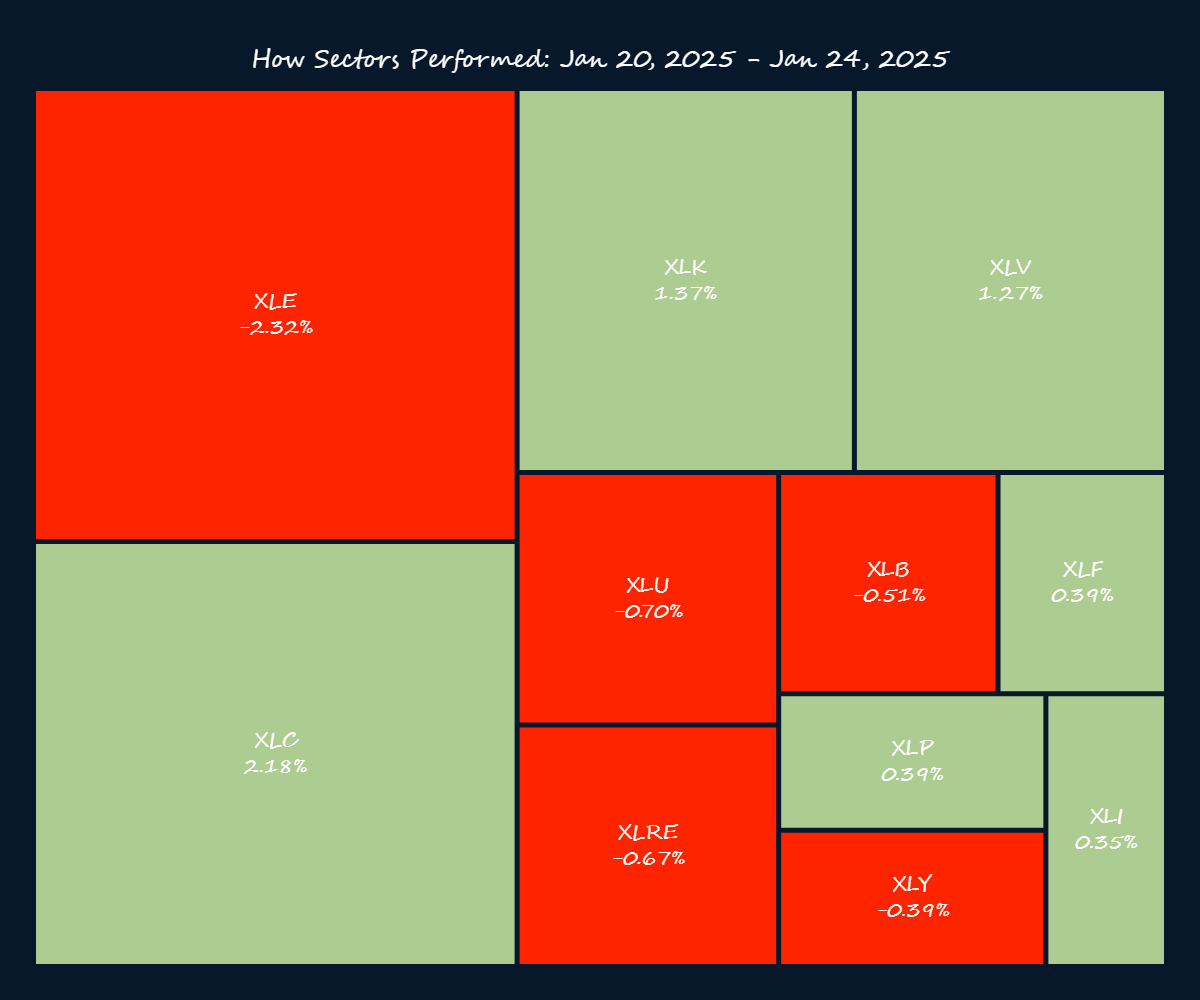

Energy was the worst-performing sector this week after a few weeks of stellar gains. It lost -2.32%. Communications services was the best-performing sector gaining 2.18%.

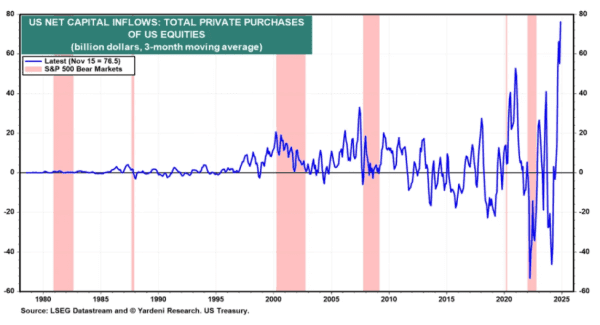

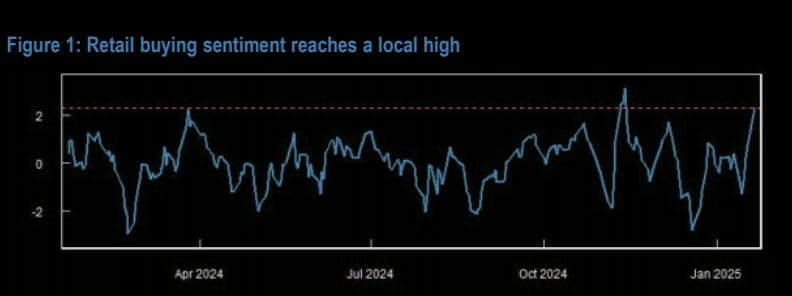

There are growing concerns among analysts that stocks are due a correction very soon. Some point to an increase in influx of retail trading both foreign and domestic.

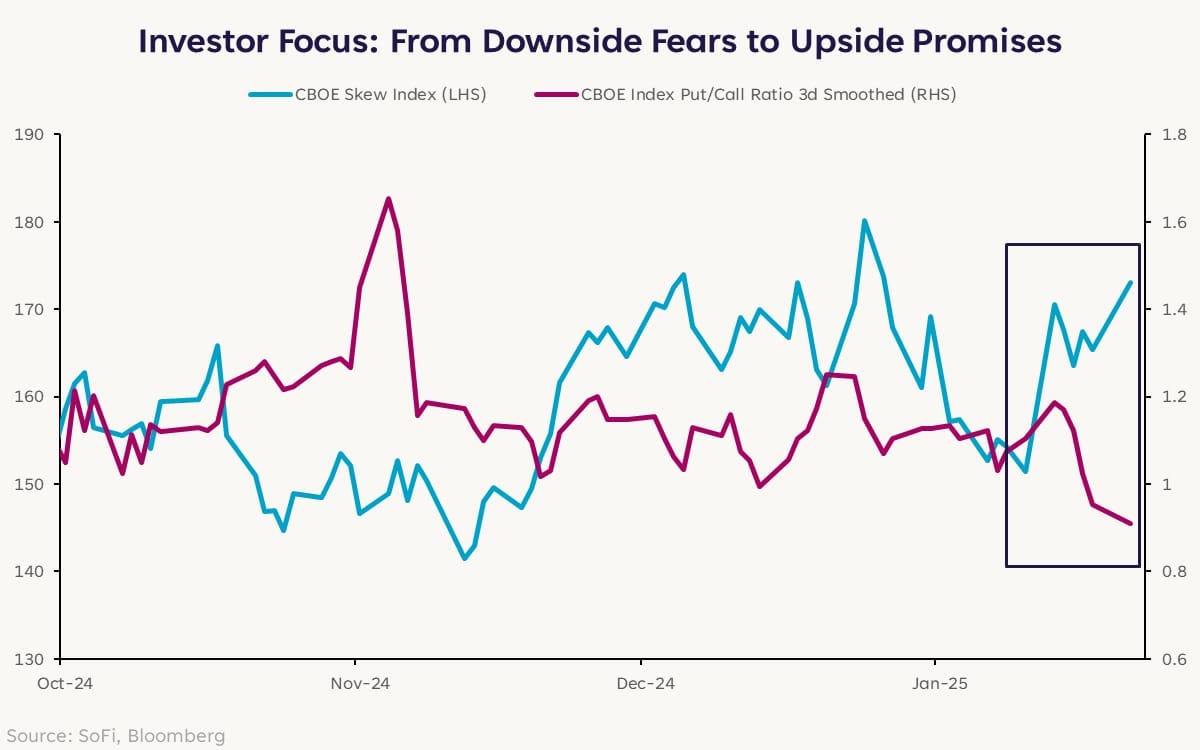

Others point to a rise in the CBOE skew, and a deviation between the VIX and VVIX. The problem with all these indicators is that they say nothing about timing.

I would note that VIX is usually too late to predict a decline and so is the put-call ratio, so if there’s a signal here it is probably SKEW and VVIX which are both worryingly high implying people are buying VIX puts!

💰 Bond Markets

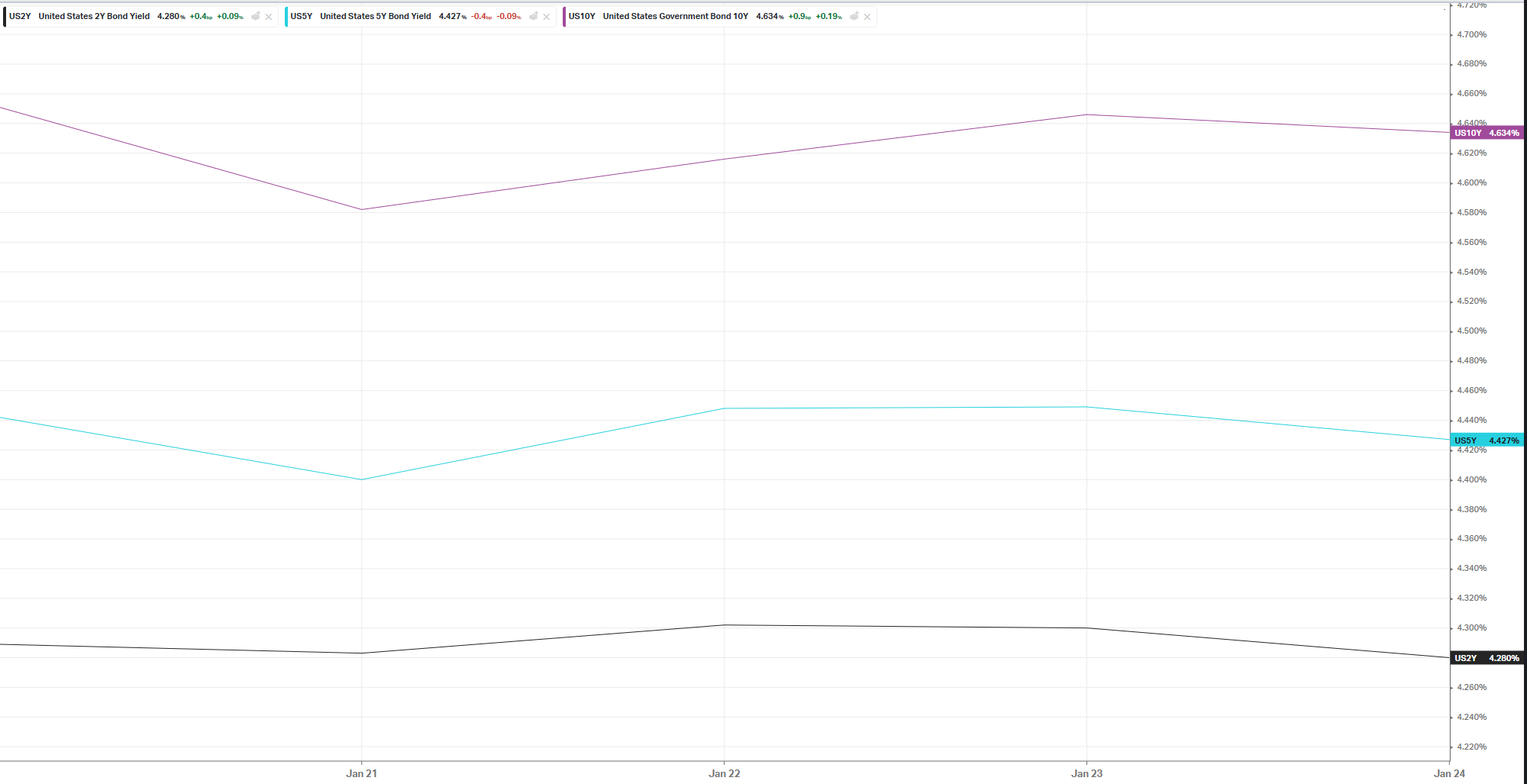

Bonds have finally budged since no tariffs were announced and this helped the dollar sell-off. Trump said that tariffs on Mexico and Canada of about 25% could be put into place by Feb 1st so bonds started to rise again on Wednesday. The Fed meeting this week is likely to lean towards a dovish hold which could help bonds (and depress yields further).

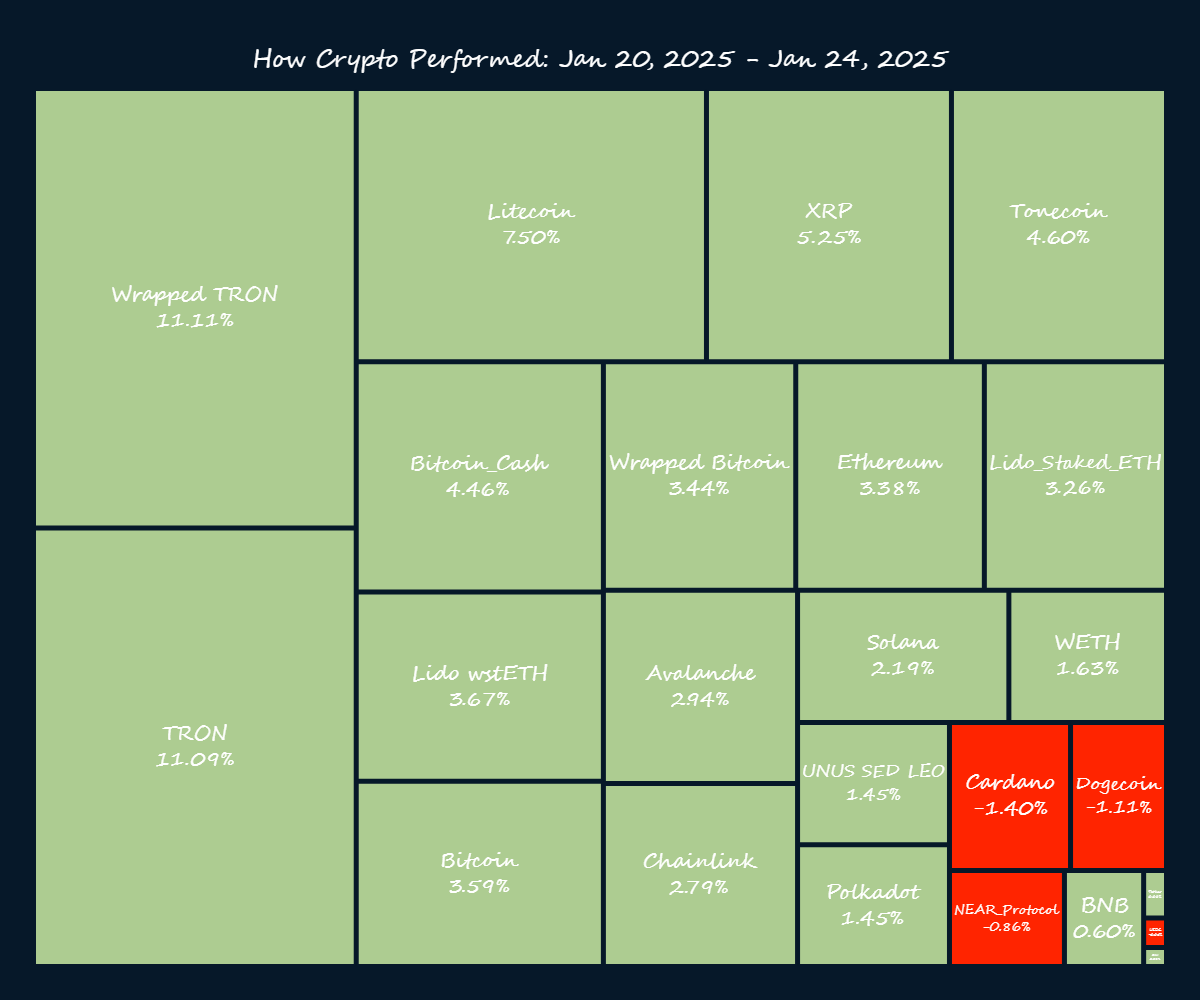

₿ Crypto

Crypto continued to rally this week even though some coins like Cardano and Doge dropped by more than 1%. Trump passed an executive order to form a crypto working group and appointed Senator Cynthia Lummis as chair of the Senate Banking Subcommittee on Digital Assets.

Some of the key goals for this group are to help craft a regulatory framework for cryptocurrencies and evaluate the creation of a digital asset stockpile. Some of the key members of this group include the SEC, CFTC, and the Treasury. Additionally, large crypto-related companies are also fighting for seats within the group to assist in helping the crypto space flourish. —Bankless

The SEC chair launched a crypto task force to develop crypto regulation.

The announcement noted that the SEC “relied primarily on enforcement actions to regulate crypto” but is now taking a different approach, creating a more collaborative environment. The task force will be led by Hester Peirce, SEC Commissioner appointed by Donald Trump, who will assist in forming the regulatory framework for the crypto space. —Bankless

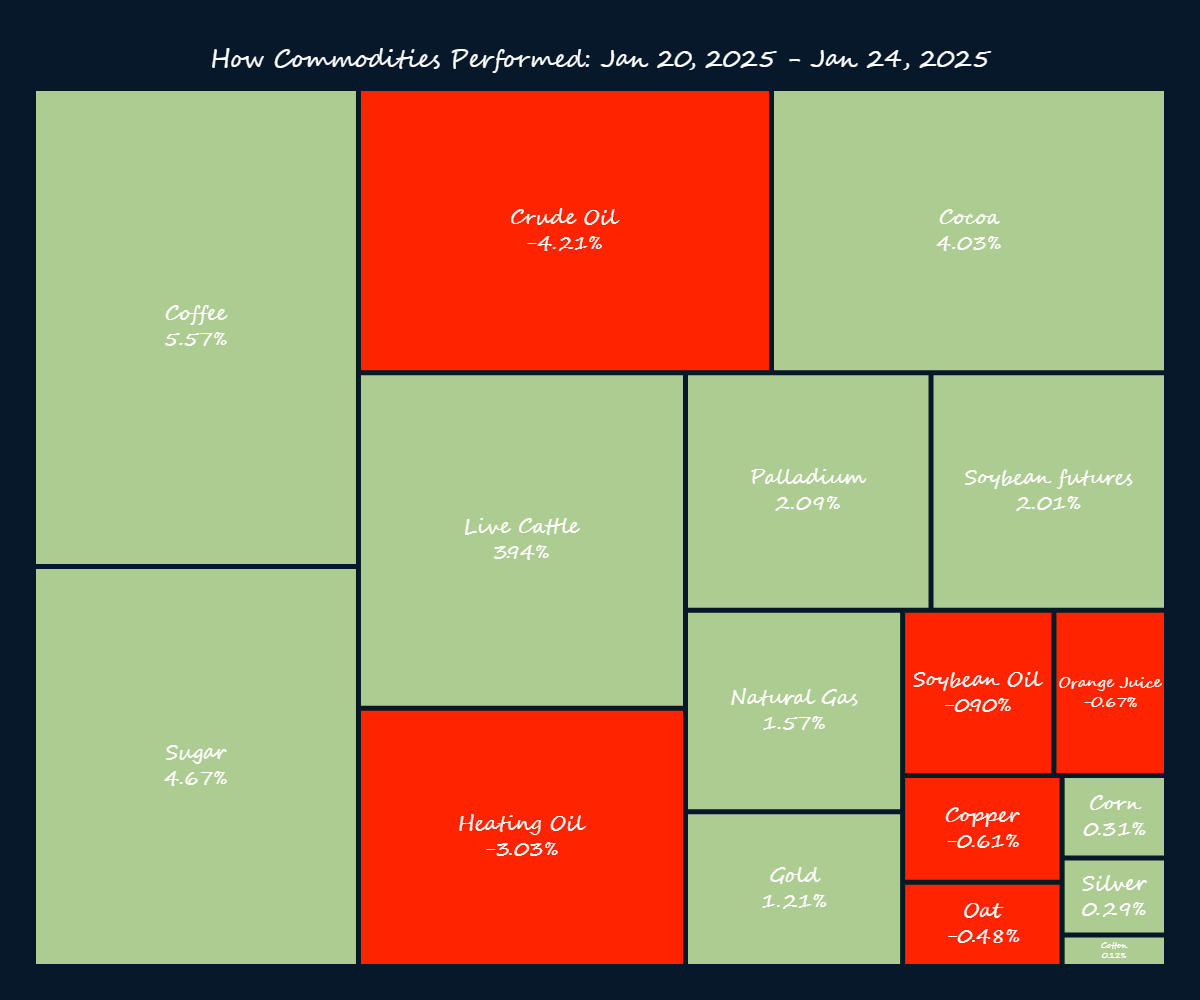

⛽ Commodities

Oil was already on a decline when Trump, in an address to Davos, put pressure on OPEC and Saudi Arabia to increase output (to lower prices) to pressure Russia into a peace treaty with Ukraine. OPEC are unlikely to do this but speculators went with it anyway. Oil closed the week at 74.50 and the EIA report showed that oil inventories continue to decline (for the 8th week) which could help support the price.

NatGas found support at $3.7 and rallied to $4. Gold was higher due to fiscal concerns from Trump’s proposed tax cuts. Cocoa continued to rally due to supply-side factors particularly low output in Ghana. Copper declined after it was revealed there would be no tariffs.

🤝 Macroeconomics

🇬🇧 UK

Things have calmed down in the UK now that global yields are declining. Fiscal concerns may continue to come up as bond investors keep a close eye on developments. This week, it was reported that Public Sector Net Borrowing increased to 17.8B.

🇺🇸 US

Here is a succinct summary of Trump’s policies and executive orders. (Source)

Immigration and Border Security

Reinstatement of the "remain in Mexico" policy, also known as the Migrant Protection Protocols.

End to the "catch and release" policy for illegal immigrants.

Trump’s administration will not recognize automatic birthright citizenship for children born to illegal immigrant parents, challenging the 14th Amendment.

Designating cartels as foreign terrorist organizations is being pursued.

Pausing refugee resettlement.

Law Enforcement and Criminal Justice

Reinstatement of the death penalty for certain crimes against federal agents.

The Attorney General is directed to seek capital punishment for the murder of law enforcement officers and for capital crimes committed by illegal immigrants.

Pardons issued for approximately 1,500 people charged in connection with the January 6th Capitol breach.

Investigations into the "weaponization" of the Department of Justice and other agencies.

Economic Policy

Directing executive departments and agencies to deliver emergency price relief, including expanding the housing supply, eliminating administrative expenses in healthcare, and removing requirements that raise the costs of home appliances7.

Abolishing "harmful, coercive ‘climate’ policies" that increase the cost of food and fuel.

Establishing an External Revenue Service to collect tariffs from foreign businesses.

Examining unfair trade relationships and currency policies with other countries9.

Considering imposing tariffs on Canada and Mexico, as well as on China if a TikTok deal is not approved.

A plan to impose a universal tariff on any business doing business in the United States.

Energy Policy

Streamlining permitting, loosening regulations, and building critical infrastructure such as pipelines.

Restoring oil and gas leasing on 13 million acres in Alaska’s National Petroleum Reserve.

Lifting restrictions on offshore drilling.

Eliminating electric vehicle subsidies and state fuel emissions waivers.

Withdrawing from the Paris Climate Accord.

Government Operations

Directing all federal workers to return to in-person work.

Establishing a new Department of Government Efficiency (DOGE) with a focus on software modernization.

A freeze on bureaucrat hiring except in essential areas16.

Social Issues

Ending federal programs and preferences based on race, sex, gender or other immutable characteristics.

Defining a female as “a person belonging at conception to the sex that produces the large reproductive cell,” referring to eggs.

Ending the promotion of "gender ideology".

Revoking the Biden administration’s efforts to expand Title IX to include gender identity.

Restoring the name of Mount McKinley, to its original name, William McKinley, and renaming the Gulf of Mexico, to the Gulf of America.

Free Speech and Censorship

Prohibiting federal employees from restraining US citizens’ free speech.

Directing the Attorney General to prepare a report to address abuses against citizens' free speech under the previous administration.

The policy that government censorship is “intolerable in a free society”.

Foreign Policy and International Agreements

Ending negotiations regarding the WHO's global pandemic treaty.

Withdrawing the United States from the World Health Organization (WHO).

Reevaluating and realigning United States foreign aid2.

The application of the Protecting Americans From Foreign Adversary Controlled Applications Act to TikTok.

Instructing the Secretary of State to inform the top ranks of the WHO and the United Nations about the withdrawal.

Revocation of Previous Orders

A large number of Biden's executive orders were revoked, covering areas such as racial equity, COVID-19 response, climate change, and diversity and inclusion initiatives.

🇨🇦 Canada

Canadian inflation declined. The yearly figure is currently at 2% and the BoC is expected to cut by 25bps this week.

🇯🇵 Japan

The BoJ hiked by 25bps as expected, but the initial USDJPY move lower was bought into after it became clear that the BoJ intended to hold rates at 0.5% for a long period. It was a dovish hike, in other words. The rate hike is not big enough to justify a return of foreign capital back home but late in the year, we will have the wage negotiations and more inflation data which could change the BoJ’s stance.

🇪🇺 EU

This week we have the ECB who are expected to cut by 25 bps. Services inflation is proving sticky in the EU and Lagarde did comment about it, but that shouldn’t affect their stance. Expect Lagarde to say that the ECB will remain data-dependent.

👁️ Media Stories

I’m sure you’ve heard enough about DeepSeek by now. A cheer for quants! I like that story because it shows that winning is about strategy and not resources, which is a key theme in Chinese military philosophy going back thousands of years. It inspires me to wonder what more I can do with the resources I already have.

🕵🏾♂️On my Radar

The main thing to keep an eye on this week is forward guidance from the various central banks and the US PCE figure.

📁 Docket

I’m still reading a lot of crypto papers. The following paper is applies ML to crypto trading (random forests, SVM) but I really hate these kinds of papers because they usually overfit and you can’t create tradeable systems out of them. This is the kind of slop people write for academic purposes but no one really uses them in the real world (hence why I don’t post about such stuff).

Another example of this kind of quant work is the paper below which tries to show that momentum has some idiosyncratic underpinnings (???).

But the following survey is giving me ideas.

🎶 Music

My favorite band is a lesser-known British duo called Aquilo. I find their music very authentic and unique.

🔖 Theoretical Stuff

One of the first things they teach you in Stochastic Calculus is about the Weistrass function. It is everywhere continuous but nowhere differentiable similar to Stochastic processes. But unlike a Stochastic process which is based on random variables, the Weistrass function is deterministic. Still, it serves as a good starting point to understand undifferentiability. Here’s a good intro to the function.

Thank you for reading!

Feedback and criticism welcomed.